Don't they?

After a previous posting on the junior mining index, the obvious question was: do juniors outperform majors? Do they consistently do so? Do juniors also outperform precious metals over the long haul ? There is at least one thing for sure:

Large Miners underperform precious metals

There is plenty of evidence that major gold stocks could not keep up with the rising price of gold. Measured by the HUI/Gold or XAU/Gold metric, major gold stocks manifestly lost track of the gold price evolution on two occasions (See refs: 1, 2):

Precious metal mining indices (as HUI or XAU) are composed of mining majors only. So what about junior miners? Do they on average perform any better than large miners? Do they consistently outperform ?

In a previous posting (Ref 4) I have been checking the MVGDXJ, the benchmark index used by the popular GDXJ junior precious metal mining ETF (discussed in an earlier posting: ref. 5, 6).

Putting 2 and 2 together

The graph below compares the MVGDXJ benchmark index to the Philadelphia Gold & Silver mining index (symbol: XAU). This broad based index of major PM miners ends 2003 at 108.8 while the MVGDXJ is set to start at 1000 that day. The XAU gets a 9% advantage to facilitate the 10:1 scaling.

Juniors retreat

December 2003 marks the end of the primary gold bull phase, whereby miners had been outperforming gold bullion during its initial slow ascent to just over $400/oz. Gold is more or less flat during most of 2004 without any meaningful pullback. Yet miners linger on lacklustre, not participating in the general stock market recovery after the dotcom bust. By end December 04, gold finally gains a timid 4.4%. Too little to please gold mine investors, who are sending the XAU gold majors south by 15%. Junior mining investors are off worse and get a 23% haircut.

Juniors outperform

The year 2005 proves better for bullion with a 17.8% rise to $513 by end December. Both junior mining companies as large miners outperform the rise of gold bullion over 2005, with a 43% and a 37% rise respectively. Juniors outperform majors, but not to the extent as to compensate for earlier malperformance. Junior mining investors have to wait one more year to see this happen. Juniors continue outperforming majors into the summer of 2007 with the MVGDXJ posting a gain of 130% since inception, peaking at 2302. The XAU has been dragging itself up to 158 that same July 23, 2007, posting a more modest gain just over 45% since end Dec-03. In the mean time gold bullion has risen to $682/oz, or over 63% up as compared that same date. Major miners couldn't catch up with bullion, while juniors ran ahead.

August - November 2007 marks the end of an era of junior mining outperformance. Over the summer, the first clouds start packing above the sub-prime mortgage segment. Mortgage brokers that are history by now, are vigorously confirming how well they are financed. Gold miners, both juniors and majors suffer along during the correction, in spite of gold holding up well and breaking both the $700 and the €500 barriers in September. The discomfort subsides in autumn and -with gold bullion steaming up above $800 towards end November- the MVGDXJ puts down a new peak at 2542, a progress of 10.4% compared to the summer peak. The XAU makes it to 189, an increase of 19% over the same time span. Gold bullion has more than doubled since end 2003, while the junior mining posts a 154% progress, against 73% for the majors of the XAU.

Bullion outperforming all

Crude oil and gold continue posting records, with bullion breaking the Jan 1980 ATH on January 3, 2008 to peak on March 17 at $1011. In the winter months of 2008, it had become clear that financials had got themselves in more trouble than they wanted to admit. Juniors depending on credits or capital raising suffered more than major miners seeing their gross margins improve. The XAU sets down a new high at 206.4 as bullion passes the $1000 mark, the MVGDXJ hardly equals its July 2007 level at 2308. None of the mining segments is outperforming bullion, having progressed by close to 150%. Juniors gave back their advantage while majors could only regain some territory lost to juniors, yet kept on underperforming gold bullion.

Shorters' paradise

With hindsight we know worse was to come. The autumn 2008 stock market implosion has sliced and diced junior miners without mercy. The MVGDXJ index lost over 80% as compared to its November 2007 peak to bottom below 500 on November 20, not even one year after its peak. Junior miners had fallen back to half their Dec 2003 value in the carnage, despite gold bullion still 70% above the Dec 2003 level during the heat of the panic. The XAU bottoms at 70 that day, about sliced in three and posting a loss of about 33% as compared to the Dec-2003 level.

Recovery

Juniors are far more volatile and brilliant outperformance may turn into a miserable swoon, as stock markets get slain. As soon as the hurricane weathered, majors were the first to recover as gold rallied higher, regaining much of its 30% loss by March 2009. Yet, junior miners quickly picked up steam after majors headed forward and their recovery proved more vigorous. The SPX sliding back to its previous panic bottom in March 09 proved but a temporary setback for both the junior and major segments. Miners were supported by strong gold prices at that time. The summer doldrums of 2009 sent gold back 7 to 8%, bottoming above $900. The junior miners suffered more, which translated in a 24% loss, while majors gave up less than 20%. Any gold retreat causes a major swoon for miners, leveraging the loss of bullion downwards.

In early December 2009, through gold rallies and corrections, juniors miners regained the territory lost to majors during the market meltdown and effectively continue outperforming large miners.

The end of year rally lost steam and gold made a retreat as we entered the second decade, bottoming in early February above $1050. This 12.7% gold correction translated in a 22.5% loss for the XAU majors and a 25.6% loss for the MVGDXJ junior mining index. But juniors prove resilience: rallies are stronger. Despite setbacks during the SPX general market correction from early May to July 2010 and gold weakness in early summer, the MVGDXJ junior index went on rallying later in summer. By end Sep 2010, the previous Nov 07 high was passed. The MVGDXJ peaked on Jan 3 at 3216 over six fold its panic bottom level and leaving the major mining index behind.

Over the long haul, the MVGDXJ fell little short in keeping up with bullion. The XAU made it to 226.6 on new year's eve, having just more than doubled since Dec 2003, while gold bullion has risen over threefold on that seven year time span.

Current situation

This year started as a copycat of 2010 with a four week January gold retreat. Surprised to see the January 25 correction bottom deeper for the MVGDXJ ? Unlike last year, gold bullion performs erratically with massive future positions driving the market. The same accounts even more for silver, with dangerously high short positions. Over the last year, the underlying trend for silver has been more bullish than for gold. Silver miners have outperformed gold miners, yet they couldn't keep up with the rising silver price. On balance precious metal price volatility is not favourable for miners. Gold has repeatedly crossed the $1400 lately. On the first occasion, miners rallied with the XAU passing the 225 mark on Dec 3. On Feb 22, gold passed the $1400 threshold again after the January correction; yet the XAU index actually posted a small loss and closed at 209.3 that day. The situation for the MVGDXJ was parallel on these days with 3209 on Dec 3, 2010 against 3101 last Feb 22. Investors demand ever higher gold prices just to keep them happy with holding on to their gold mining stocks.

Outlook

Junior miners as a group are more correlated with the general stock market than majors. They also tend to leverage the variations of the gold price more dynamically, as proved by the vigorous rallies we witnessed.

An important drive for individual junior miners and explorers is the probability of them being acquired by major gold miners in search of extending their reserve and resource base. Several important deals have been made lately: Kinross bought Redback, Goldcorp bought Andean and lately Newmont is targeting Fronteer (Ref. 7). These acquisitions have been driving junior valuations higher. Deals are typically being concluded as the outlook for the gold price is favourable.

A take-over of some successful explorer or junior miner spurs interest in the junior segment and the spill-over effect tends to lift valuations across the board. Few explorer-developers make it on their own and turn into emerging producers. Trump cards are: 1) a reserve base large enough for decades of production; 2) cost reduction as production is scaled up; 3) attain a profitable production avoiding the need for capital raises or high debt burden.

There are an awful lot more investment considerations on junior mining and precious metal explorers, going far beyond the message I want to convey here. You'll find some further reading below.

Note: the above graph was last updated in the blogpost "The MVGDXJ Junior Mining Index"

References:

1: Decades of underperformance

2: Did you say leverage?

3: Silver miners underperforming silver bullion?

4: A Junior Gold Mining Index

5: Investing directly in juniors or through the GDXJ ETF?

6: GDXJ or GLDX, what to choose in the Gold Exploring Realm?

7: Newmont buys out Fronteer: what's next in the gold mining sector

8: Post 2008 lows of gold miners relative to gold

Further reading:

Jeff Nielson (2009): Investment Check-list for Precious Metals Miners (part I)

Jeff Nielson (2009): Investment Check-list for Precious Metals Miners: part II

Sid Rajeev (2010): An investing checklist: Five steps to narrow the field

After a previous posting on the junior mining index, the obvious question was: do juniors outperform majors? Do they consistently do so? Do juniors also outperform precious metals over the long haul ? There is at least one thing for sure:

Large Miners underperform precious metals

There is plenty of evidence that major gold stocks could not keep up with the rising price of gold. Measured by the HUI/Gold or XAU/Gold metric, major gold stocks manifestly lost track of the gold price evolution on two occasions (See refs: 1, 2):

- at the end of the 20 year bear market in 2000, gold stocks ultimately got shattered as gold bullion bottomed at $250/oz,

- during the autumn 2008 market implosion, major gold stocks dropped vastly more than bullion, which bottomed out barely above $700, losing about 30%, relative to the March-08 peak above $1000/oz.

Precious metal mining indices (as HUI or XAU) are composed of mining majors only. So what about junior miners? Do they on average perform any better than large miners? Do they consistently outperform ?

In a previous posting (Ref 4) I have been checking the MVGDXJ, the benchmark index used by the popular GDXJ junior precious metal mining ETF (discussed in an earlier posting: ref. 5, 6).

Putting 2 and 2 together

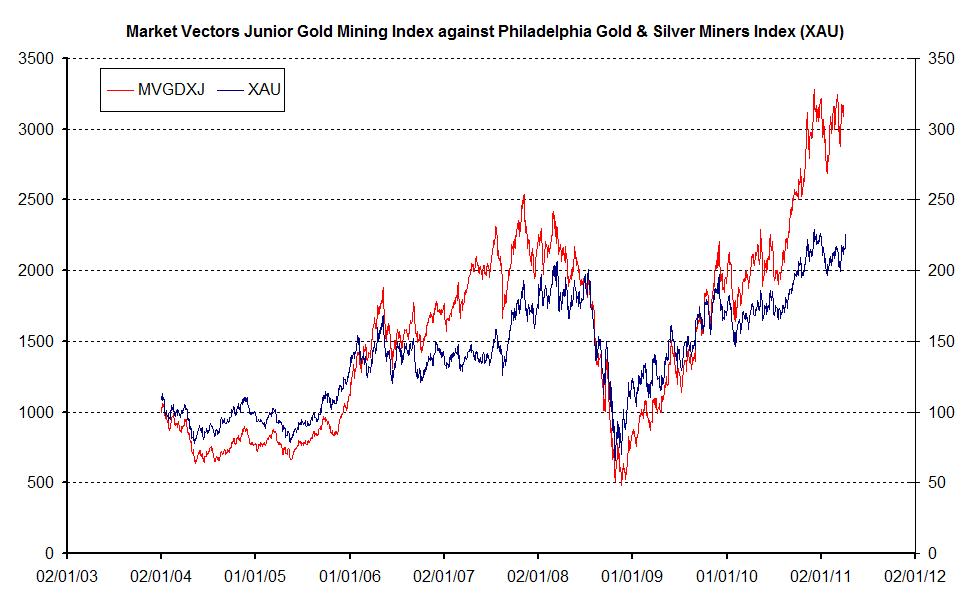

The graph below compares the MVGDXJ benchmark index to the Philadelphia Gold & Silver mining index (symbol: XAU). This broad based index of major PM miners ends 2003 at 108.8 while the MVGDXJ is set to start at 1000 that day. The XAU gets a 9% advantage to facilitate the 10:1 scaling.

|

| Market Vectors GDXJ benchmark index (red - left axis) against the broad Philadelphia Gold & Silver miners index (blue - right axis) - Data run from Dec 31, 2003. XAU data are scaled up to make them comparable to the MVGDXJ. - Click to enlarge |

December 2003 marks the end of the primary gold bull phase, whereby miners had been outperforming gold bullion during its initial slow ascent to just over $400/oz. Gold is more or less flat during most of 2004 without any meaningful pullback. Yet miners linger on lacklustre, not participating in the general stock market recovery after the dotcom bust. By end December 04, gold finally gains a timid 4.4%. Too little to please gold mine investors, who are sending the XAU gold majors south by 15%. Junior mining investors are off worse and get a 23% haircut.

Juniors outperform

The year 2005 proves better for bullion with a 17.8% rise to $513 by end December. Both junior mining companies as large miners outperform the rise of gold bullion over 2005, with a 43% and a 37% rise respectively. Juniors outperform majors, but not to the extent as to compensate for earlier malperformance. Junior mining investors have to wait one more year to see this happen. Juniors continue outperforming majors into the summer of 2007 with the MVGDXJ posting a gain of 130% since inception, peaking at 2302. The XAU has been dragging itself up to 158 that same July 23, 2007, posting a more modest gain just over 45% since end Dec-03. In the mean time gold bullion has risen to $682/oz, or over 63% up as compared that same date. Major miners couldn't catch up with bullion, while juniors ran ahead.

August - November 2007 marks the end of an era of junior mining outperformance. Over the summer, the first clouds start packing above the sub-prime mortgage segment. Mortgage brokers that are history by now, are vigorously confirming how well they are financed. Gold miners, both juniors and majors suffer along during the correction, in spite of gold holding up well and breaking both the $700 and the €500 barriers in September. The discomfort subsides in autumn and -with gold bullion steaming up above $800 towards end November- the MVGDXJ puts down a new peak at 2542, a progress of 10.4% compared to the summer peak. The XAU makes it to 189, an increase of 19% over the same time span. Gold bullion has more than doubled since end 2003, while the junior mining posts a 154% progress, against 73% for the majors of the XAU.

Bullion outperforming all

Crude oil and gold continue posting records, with bullion breaking the Jan 1980 ATH on January 3, 2008 to peak on March 17 at $1011. In the winter months of 2008, it had become clear that financials had got themselves in more trouble than they wanted to admit. Juniors depending on credits or capital raising suffered more than major miners seeing their gross margins improve. The XAU sets down a new high at 206.4 as bullion passes the $1000 mark, the MVGDXJ hardly equals its July 2007 level at 2308. None of the mining segments is outperforming bullion, having progressed by close to 150%. Juniors gave back their advantage while majors could only regain some territory lost to juniors, yet kept on underperforming gold bullion.

Shorters' paradise

With hindsight we know worse was to come. The autumn 2008 stock market implosion has sliced and diced junior miners without mercy. The MVGDXJ index lost over 80% as compared to its November 2007 peak to bottom below 500 on November 20, not even one year after its peak. Junior miners had fallen back to half their Dec 2003 value in the carnage, despite gold bullion still 70% above the Dec 2003 level during the heat of the panic. The XAU bottoms at 70 that day, about sliced in three and posting a loss of about 33% as compared to the Dec-2003 level.

Recovery

Juniors are far more volatile and brilliant outperformance may turn into a miserable swoon, as stock markets get slain. As soon as the hurricane weathered, majors were the first to recover as gold rallied higher, regaining much of its 30% loss by March 2009. Yet, junior miners quickly picked up steam after majors headed forward and their recovery proved more vigorous. The SPX sliding back to its previous panic bottom in March 09 proved but a temporary setback for both the junior and major segments. Miners were supported by strong gold prices at that time. The summer doldrums of 2009 sent gold back 7 to 8%, bottoming above $900. The junior miners suffered more, which translated in a 24% loss, while majors gave up less than 20%. Any gold retreat causes a major swoon for miners, leveraging the loss of bullion downwards.

In early December 2009, through gold rallies and corrections, juniors miners regained the territory lost to majors during the market meltdown and effectively continue outperforming large miners.

The end of year rally lost steam and gold made a retreat as we entered the second decade, bottoming in early February above $1050. This 12.7% gold correction translated in a 22.5% loss for the XAU majors and a 25.6% loss for the MVGDXJ junior mining index. But juniors prove resilience: rallies are stronger. Despite setbacks during the SPX general market correction from early May to July 2010 and gold weakness in early summer, the MVGDXJ junior index went on rallying later in summer. By end Sep 2010, the previous Nov 07 high was passed. The MVGDXJ peaked on Jan 3 at 3216 over six fold its panic bottom level and leaving the major mining index behind.

Over the long haul, the MVGDXJ fell little short in keeping up with bullion. The XAU made it to 226.6 on new year's eve, having just more than doubled since Dec 2003, while gold bullion has risen over threefold on that seven year time span.

Current situation

This year started as a copycat of 2010 with a four week January gold retreat. Surprised to see the January 25 correction bottom deeper for the MVGDXJ ? Unlike last year, gold bullion performs erratically with massive future positions driving the market. The same accounts even more for silver, with dangerously high short positions. Over the last year, the underlying trend for silver has been more bullish than for gold. Silver miners have outperformed gold miners, yet they couldn't keep up with the rising silver price. On balance precious metal price volatility is not favourable for miners. Gold has repeatedly crossed the $1400 lately. On the first occasion, miners rallied with the XAU passing the 225 mark on Dec 3. On Feb 22, gold passed the $1400 threshold again after the January correction; yet the XAU index actually posted a small loss and closed at 209.3 that day. The situation for the MVGDXJ was parallel on these days with 3209 on Dec 3, 2010 against 3101 last Feb 22. Investors demand ever higher gold prices just to keep them happy with holding on to their gold mining stocks.

Outlook

Junior miners as a group are more correlated with the general stock market than majors. They also tend to leverage the variations of the gold price more dynamically, as proved by the vigorous rallies we witnessed.

An important drive for individual junior miners and explorers is the probability of them being acquired by major gold miners in search of extending their reserve and resource base. Several important deals have been made lately: Kinross bought Redback, Goldcorp bought Andean and lately Newmont is targeting Fronteer (Ref. 7). These acquisitions have been driving junior valuations higher. Deals are typically being concluded as the outlook for the gold price is favourable.

A take-over of some successful explorer or junior miner spurs interest in the junior segment and the spill-over effect tends to lift valuations across the board. Few explorer-developers make it on their own and turn into emerging producers. Trump cards are: 1) a reserve base large enough for decades of production; 2) cost reduction as production is scaled up; 3) attain a profitable production avoiding the need for capital raises or high debt burden.

There are an awful lot more investment considerations on junior mining and precious metal explorers, going far beyond the message I want to convey here. You'll find some further reading below.

Note: the above graph was last updated in the blogpost "The MVGDXJ Junior Mining Index"

References:

1: Decades of underperformance

2: Did you say leverage?

3: Silver miners underperforming silver bullion?

4: A Junior Gold Mining Index

5: Investing directly in juniors or through the GDXJ ETF?

7: Newmont buys out Fronteer: what's next in the gold mining sector

8: Post 2008 lows of gold miners relative to gold

Further reading:

Jeff Nielson (2009): Investment Check-list for Precious Metals Miners (part I)

Jeff Nielson (2009): Investment Check-list for Precious Metals Miners: part II

Sid Rajeev (2010): An investing checklist: Five steps to narrow the field

More similar papers are linked to in the top section of the list of blog articles.

No comments:

Post a Comment