As we start a new year, it's time to make an update on the situation of gold and silver miners, using the approach you also find in the 'gold miner pulse' blog page and/or the miner performance page. Those pages have been updated with fresh information as of Dec 31st, 2015.

Several more detailed articles, using a similar approach, have been published (a good read for the more long term perspective):

This blog article has a time perspective covering years or decades, but is also monitoring whether the trends observed are persisting.

Unhedged Gold miners relative to Gold bullion

During the bear market of the late 1990's, the HUI index slid below 40 in Nov 2000. Gold upheld $250 and the HUI/Gold ratio never slid as low as it has now. During the early gold bull years (2001-2003) gold miners outperformed bullion and the HUI/Gold ratio got back to its Dec 1996 starting level by autumn 2003. From autumn 2003 till the spring of 2008 the curves are almost coinciding, with the HUI index at about half of the price of gold in $/Oz. By now the HUI index (barely upholding 100) has lost five fold relative to gold.

Even before gold made its all time high above $1900 in Aug/Sep 2011, HUI/Gold had been retreating, with fresh lows set after any gold recovery failed. Recently the bear market logic: a non-proportional relationship between HUI and Gold has been described, which shows why HUI/Gold (or for that purpose Gold/XAU) has become less significant as a valuation parameter. Graphs in this article also were updated with fresh information as of Dec 31, 2015.

If there's any perspective for a future recovery of the gold miners, it must be that the residuals relative to the least squares prediction have turned positive lately. The HUI index and HUI/Gold were lower during August gold slide than they are now for the same gold price value. In order for that recovery to take root, precious metals ultimately need to strengthen durably.

After the brutal slide mid July, the SIL/Silver ratio slid below 1.32 from 1.63 early July, with fresh absolute lows on a weekly basis. The silver roller coaster ride, first lifted SIL/Silver off its recent low only to plunge back on account of precious metals sliding during the stock market recession. Silver staying above $16/Oz could stabilize silver miners: but things work out differently.

While the white metal slid below $14, to a new post 2009 low, SIL/Silver finally gave way after mid Dec and slid to 1.339 below its 50dma and into bearish territory. The brief recovery attempt before Xmas was temporary.

NOTE: There has been a 3:1 consolidation (or reverse split) on SIL. Historic values for SIL/Silver in the graphs have been changed accordingly.

SIL/Silver flagged out 2014 at 1.68. As with HUI/Gold, 2015 started with silver miners outperforming the white metal. SIL/Silver was approaching the top level of the late November bounce. But silver has some work to do, after sliding 20% over 2014, where gold almost held ground. Silver miners did not share the wakening enthusiasm gold miners have enjoyed. SIL/Silver first kept flirting with its 50 dma level and then broke down, having dropped below its mid December '14 bottom on Tuesday, Mar 10. Silver has been quoting at a critical level, with most miners producing below the all sustaining costs.

Unlike the January recovery for gold miners, that of silver miners has been half-hearted, with SIL/Silver during the subsequent March miner slump digging to a yet a lower minimum. Silver unable to make any meaningful recovery from its post 2009 minimum is the main culprit.

During 2015, the 200 dma constantly keeps above the 50 dma, which confirms the continuation of the declining trend. SIL/Silver briefly breaks above its 200 dma in June 2015. Silver miners have been sliding well into August and keep oscillating at a much lower level ever since. Silver unable to uphold $15 has been a set back for silver miners.

How we got there:

"Silver miners upholding better than gold miners" ought to be reformulated: "The slide of silver miners is more often interrupted by a recovery than that of gold miners on their seemingly fatal path to perdition."

Extreme losses of silver with wild intraday swings causes the SIL/Silver ratio to behave erratically. Yet the systematic downtrend of SIL/Silver is more recent than that of HUI/Gold observed for gold miners. The one and three years moving averages initially are close to one another and a lot more flat than what we find for HUI/Gold.

However, it should be borne in mind that most often, silver miners have important income streams from other metals. Silver naturally occurs either in combination with copper or with lead and tin. Some gold miners also have an important secondary silver production.

The brutal 2014 Halloween slide brought SIL/Silver below its December 2013 bottom. After the brief November bounce, the mid December 2014 slide shows we are still searching for the true cycle bottom. SIL/Silver flagged 2014 out at 1.68.

Canadian Gold and Silver Mining indices

How gold miners are performing is shown by the capitalization weighed gold miners index of stocks included in the Gold Miner Pulse database (yellow diamond symbols). Note that most quotes are in CAD, which has been fluctuating to the USD. By end 2012, before the leg down set in, the silver miners index (blue square symbols) was best on its way to gaining back its initial level. Yet, mid December 2014 it set a new bottom. Silver miners lagged during the January recovery. After the Friday Mar 6 wash-out on precious metals, the silver miners index has been down over 2015. The mid May recovery has only temporarily been alleviating the pain. For 14 consecutive weeks, precious metals have been grinding lower with the late July silver plunge below $15/Oz particularly harmful for the miners. The mid August recovery was short-lived. Early Oct, the indices seemed having completed a double bottom formation, much alike the Nov/Dec 2014 double bottom, but we aren't out of trouble yet: precious metals continue weakening since mid October, quenching the miner recovery.

The third index added is an equally weighted index of all (silver and gold) miners from the GMP database. Because of its simple weighing scheme, comparing this index to the capitalisation weighted indices gives a fair idea of how junior miners and explorers fare as compared to the large miners. The equal weight index used to correlate well with the silver miners index: in comparison to the gold mining bellwethers, silver miners are mid caps or small caps. Since recovering from the July 2012 secondary low, silver miners have been outperforming gold miners, with the junior tilted equal weight index mimicking gold miners rather than silver miners (as it used to before). Juniors and explorers have been recovering some of their losses relative to the gold mining majors.

How we got so deep into trouble is best illustrated when showing a long term graph of those capitalization weighed miners indices. It also puts both the short-lived August 2013 and past March and June 2014 or Jan 2015 miner revivals in perspective.

The silver miners index rose till 1400 in April 2011, peaking three weeks earlier than did the silver price. After bottoming on June 26, 2013, the gold miners index had recovered, yet in December 2013 was back down again threatening to take out the June low. The equal weight (junior dominated) miners index effectively made another low in December.

Performance of the Canadian miners of the Gold Miner Pulse database

The performance calculated is relative to the start of the calculation of the GMP based gold miners and silver miners index on Nov 19, 2010. For your information: gold closed at $1342/oz and silver at $27.07/oz on that day.

On Dec 31, 2015 the median loss for the miners in the database stands at 83.6%, while the average loss is 72.2%. The median is the value observed in the middle of the distribution.

The average is tilted higher (less negative) because of the asymmetry in the performance distribution, slanted towards the few gains we've left. There now are 33 miners down 90% or more with 23 thereof down over 95%. Only 5 miners are up since Nov 2010.

Since the previous evaluation on Dec 11, there are 38 miners advancing against 44 declining, with the remainder (12) almost flat: within a +1% range.

Click any of the graphs to view them at true size

A few miners are no longer covered on the GoldMinerPulse site, but I've kept them on board, e.g. Chesapeake Gold. Newcomers are AR, BTG, CMB, CUU, DPM, GCM, IMG, LSG, NCQ, TXG, OR and OGC (Oceana Gold), making the total equal 94.

Several more detailed articles, using a similar approach, have been published (a good read for the more long term perspective):

- Miners relative to precious metals: a tactical approach; (July 2, 2012)

- Miners relative to precious metals: An update on 2012 (Jan 13, 2013)

- Anatomy of a gold miner bear market (Dec 30, 2013)

- Three year slide of precious metal miners (Dec 31, 2014)

This blog article has a time perspective covering years or decades, but is also monitoring whether the trends observed are persisting.

Unhedged Gold miners relative to Gold bullion

After the brutal slide from May till early August, the gold recovery till Aug 20 lifted HUI/Gold off its lows. Despite a mild gold pull back precious metal miners once more plunged, taking the lead in the stock market recession. The late August optimism was another bull trap, both stock markets and precious metals weakening sent miners south again, with HUI/Gold back below 0.100, at its its all-time low. Failing recoveries alternate with swoons, setting a multiple bottom formation. In October, gold market strength started translating into miner strength, but the recovery still was frail. Gold plunged to a fresh post-2011 low on Nov 27, after its partial recovery faltered well below $1100, HUI/Gold initially upheld, but the mid Dec gold slide was the step too far. Despite a brief recovery attempt before Xmas, HUI/Gold still is quoting at 0.1048 below its 50 dma into bearish territory. 2015 once more proved that predicting the market bottom is a recipe for failure.

The declining 200 dma situated quite high above both the graph and the 50 dma is a tell-tale of the preceding decline during the first half of 2015. Adding the full year graph therefore adds that different perspective.

The six month graph left behind the short January recovery, petering out in February and breaking down into a new dip for miners by mid March. HUI/Gold has failed to pierce the declining 200 dma line during its short lived uptrend: an indication that it's premature to call the end of the gold miner bear market. There is nothing left of the nascent miner enthusiasm early May. For 14 consecutive weeks, the HUI/Gold ratio has been grinding lower, with a first bottom reached early August.

How we got there:

The past year has been the continuation of a trend starting much earlier, as mining valuations had been eroding rapidly. The following graph with weekly observations covers three years: from Jan 2013 till Dec 2015. This includes the onset of the gold bear market as the support level at $1560/Oz, which had held for several years, ultimately gave way in April 2013.

Since the 3 years weekly moving average constantly is situated above the 1 year moving average, the declining trend over three years clearly started quite some time before 2013. The latest updated long term graphs of HUI/Gold can be found at Miners relative to gold: Long term charts on the HUI index. The HUI index has been calculated since 1996. Below you find an extra long term simultaneous view of the HUI index and the gold price.

|

| Unhedged Gold Miners index HUI relative to gold bullion (spot market). Daily observations over 6 months. - click to enlarge |

|

| Unhedged Gold Miners index HUI relative to gold bullion (spot market). Daily observations 2015. - click to enlarge |

How we got there:

The past year has been the continuation of a trend starting much earlier, as mining valuations had been eroding rapidly. The following graph with weekly observations covers three years: from Jan 2013 till Dec 2015. This includes the onset of the gold bear market as the support level at $1560/Oz, which had held for several years, ultimately gave way in April 2013.

|

| Unhedged Gold Miners index HUI relative to gold bullion (spot market). Weekly observations over 2013-2015 and moving averages over 1 (blue) and 3 years (red) - click to enlarge |

|

| Very long term view of the gold price ($/oz, red, left axis) and the HUI index (blue, right axis) |

Even before gold made its all time high above $1900 in Aug/Sep 2011, HUI/Gold had been retreating, with fresh lows set after any gold recovery failed. Recently the bear market logic: a non-proportional relationship between HUI and Gold has been described, which shows why HUI/Gold (or for that purpose Gold/XAU) has become less significant as a valuation parameter. Graphs in this article also were updated with fresh information as of Dec 31, 2015.

If there's any perspective for a future recovery of the gold miners, it must be that the residuals relative to the least squares prediction have turned positive lately. The HUI index and HUI/Gold were lower during August gold slide than they are now for the same gold price value. In order for that recovery to take root, precious metals ultimately need to strengthen durably.

Global X Silver Miners ETF (SIL) relative to silver bullion

After the brutal slide mid July, the SIL/Silver ratio slid below 1.32 from 1.63 early July, with fresh absolute lows on a weekly basis. The silver roller coaster ride, first lifted SIL/Silver off its recent low only to plunge back on account of precious metals sliding during the stock market recession. Silver staying above $16/Oz could stabilize silver miners: but things work out differently.

While the white metal slid below $14, to a new post 2009 low, SIL/Silver finally gave way after mid Dec and slid to 1.339 below its 50dma and into bearish territory. The brief recovery attempt before Xmas was temporary.

|

| Silver miners are observed through the GlobalX ETF : SIL. Daily observations of SIL/Silver bullion over 6 months, click to enlarge |

SIL/Silver flagged out 2014 at 1.68. As with HUI/Gold, 2015 started with silver miners outperforming the white metal. SIL/Silver was approaching the top level of the late November bounce. But silver has some work to do, after sliding 20% over 2014, where gold almost held ground. Silver miners did not share the wakening enthusiasm gold miners have enjoyed. SIL/Silver first kept flirting with its 50 dma level and then broke down, having dropped below its mid December '14 bottom on Tuesday, Mar 10. Silver has been quoting at a critical level, with most miners producing below the all sustaining costs.

Unlike the January recovery for gold miners, that of silver miners has been half-hearted, with SIL/Silver during the subsequent March miner slump digging to a yet a lower minimum. Silver unable to make any meaningful recovery from its post 2009 minimum is the main culprit.

|

| Silver miners are observed through the GlobalX ETF : SIL. Daily observations of SIL/Silver bullion over 2015, click to enlarge |

How we got there:

"Silver miners upholding better than gold miners" ought to be reformulated: "The slide of silver miners is more often interrupted by a recovery than that of gold miners on their seemingly fatal path to perdition."

|

| Silver miners are observed through the GlobalX ETF : SIL. Weekly observations of SIL/Silver bullion over 3 years, from Jan 2013 till Dec 2015 and moving averages over 1 (blue) and 3 years (red), click to enlarge |

However, it should be borne in mind that most often, silver miners have important income streams from other metals. Silver naturally occurs either in combination with copper or with lead and tin. Some gold miners also have an important secondary silver production.

The brutal 2014 Halloween slide brought SIL/Silver below its December 2013 bottom. After the brief November bounce, the mid December 2014 slide shows we are still searching for the true cycle bottom. SIL/Silver flagged 2014 out at 1.68.

Canadian Gold and Silver Mining indices

|

| Gold Miners index, Silver miners index and Equal Weight Index, base Nov 19, 2010, click to enlarge |

How we got so deep into trouble is best illustrated when showing a long term graph of those capitalization weighed miners indices. It also puts both the short-lived August 2013 and past March and June 2014 or Jan 2015 miner revivals in perspective.

|

| Long term graph of the GMP list based (and capitalisation weighed) gold (black), silver (blue) and equal weight (red) miners indices. Reference 1000 on Nov 19, 2010. - Data till Jan 08, 2016 (click to enlarge) |

The silver miners index posted a higher maximum during both the March 2014 and June to early August recovery than it did in the August 2013 recovery. The gold miners index and the equal weight index did not peak higher at any of the latest recoveries than they did in August 2013.

Performance graph

There is an important performance disparity among the gold and silver miners of the GMP database. Too many laggards seem moribund. The median (or middle) miner (with an equal number better and worse) is losing 83.6%. More than a quintuple is needed to break even.

There are 33 miners/explorers losing 90% or more, with 23 thereof down over 95%.

Performance graph

There is an important performance disparity among the gold and silver miners of the GMP database. Too many laggards seem moribund. The median (or middle) miner (with an equal number better and worse) is losing 83.6%. More than a quintuple is needed to break even.

|

| GMP Miners sorted by loss to gain since inception on Nov 19, 2010. Click to enlarge |

Only 5 miners are quoting above their Nov 2010 mark, lead by Klondex Mines and Tahoe Resources. Since a while, the performance graph is looking like a submarine, cruising at periscope depth.

Next chapter provides a more detailed analysis including the list composition.

|

| Only the top-5 performers are above break-even since Nov 19, 2010. |

Performance of the Canadian miners of the Gold Miner Pulse database

The past performance of Canadian miners included in the GoldMinerPulse database has been covered in earlier postings:

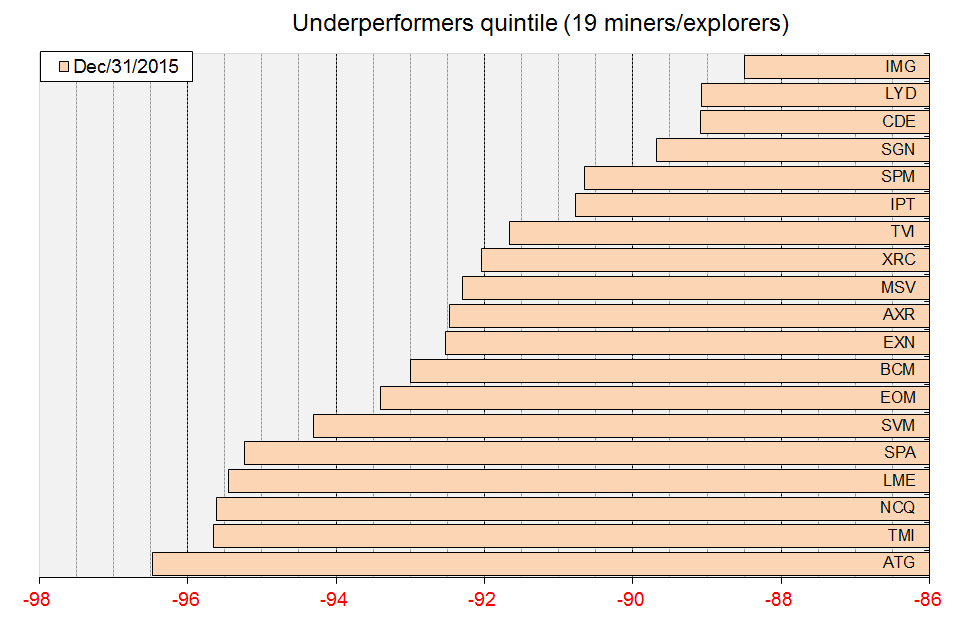

A more frequent follow-up is useful, but rather tedious. As a trade-off, here are some fresh graphs (last update see on top) on the five performance quintiles, but without any specific miner oriented comment. The symbols used are the Canadian (TSX) quotes (See also bottom table). The database contains 94 miners or explorers. The quintiles contain 19 components, apart from the fifth, which counts only 18.The performance calculated is relative to the start of the calculation of the GMP based gold miners and silver miners index on Nov 19, 2010. For your information: gold closed at $1342/oz and silver at $27.07/oz on that day.

On Dec 31, 2015 the median loss for the miners in the database stands at 83.6%, while the average loss is 72.2%. The median is the value observed in the middle of the distribution.

The average is tilted higher (less negative) because of the asymmetry in the performance distribution, slanted towards the few gains we've left. There now are 33 miners down 90% or more with 23 thereof down over 95%. Only 5 miners are up since Nov 2010.

Since the previous evaluation on Dec 11, there are 38 miners advancing against 44 declining, with the remainder (12) almost flat: within a +1% range.

Click any of the graphs to view them at true size

|

| The dreadfully poor performance of miners over the long haul is obvious, as even in the top quintile (the best 19 miners) we only have 5 advancing and gains have been dwindling |

|

| With all of the bottom quintile posting a loss over 95%: those really are the basket cases |

Comments and composition changes:

- The quoting of GBG has been suspended after the close on Sep 14, 2012 after it stopped mining at its Burnstone mine in South Africa and had to file for protection from creditors. GBG has been dropped from the GMP list.

- High river gold (HRG) leaves the selection after completing its merger with Nord Gold

- Orko Silver (OK) left the selection after the acquisition decision by CDE.

- Queenston Mining left the selection after its acquisition by Osisko.

- The quoting of Barkerville Gold has been suspended for legal reasons and as such I have withdrawn it from the list.

- Esperanza Silver Corp. (EPZ) was acquired by Alamos Gold and has been delisted on TSX

- Osisko Mining has been acquired by Yamana and Agnico Eagle. The quote has been removed.

- Plato Gold Corp (PGC) sold its mineral claims in Val d'or - Québec to Monarques Resources (MQR) and no longer actively explores

- Excellon Resources (EXN), Kirkland Gold (KGI) and Monarques Resources (MQR) were added to the quote list. They are not covered by GoldMinerPulse.

- South American Silver is renamed to Tri-Metals Mining. The new quote is TMI

- Pacific Rim Mining leaves the selection after acquisition by OceanaGold

- American Bonanza Gold Corp. (BZA) leaves the selection after its acquisition by Kerr Minerals (which now is in a merger operation with San Gold - SGR)

- San Gold has been delisted by TSX on Dec 23, 2014. The quote has been removed.

- US Silver & Gold was acquired by Scorpio Mining. The quote has been removed.

- Rio Alto Mining has been acquired by Tahoe Resources. The quote has been removed.

- Paramount Silver and Gold has been acquired by Coeur d'Alène; the quote was removed.

- Revett Minerals has been acquired by Hecla Mining. The quote has been removed.

- Aurico Gold has merged its gold mining activities with Alamos gold. The quote was removed.

- Wildcat silver was renamed to Arizona Mining, with ticker AZ

- Sunward Resources was acquired by Novacopper (NCQ). The SWD quote was removed.

- Crocodile Gold Res. has completed its merger with Newmarket Gold. The quote was removed.

- Tyhee has been suspended by TSX since mid June. I have removed the quoted.

- Silver Crest was acquired by First Majestic Silver. The quote has been removed.

- Temex Resources was acquired by Lake Shore Gold. The quote will be removed.

The quote list: If the Toronto Stock Exchange (TSX) symbols are less familiar, you find the mining or exploration company name next to the TSX symbol in the below list, former names are indicated between brackets:

| Quote | Name | Quote | Name | |

| ABX | Barrick Gold | K | Kinross Gold Corporation | |

| AEM | Agnico-Eagle Mines Limited | KDX | Klondex Mines Ltd. | |

| AGI | Alamos Gold Inc | KGI | Kirkland Gold | |

| AGQ | Arian Silver Corporation | KSK | Kiska Metals Corporation | |

| AGV | Agave Silver Ltd (Cream Min) | LME | Laurion Mineral Exploration | |

| AMG | AM Gold Inc. | LMG | Lincoln Mining Group | |

| AMM | Almaden Minerals Ltd. | LSG | Lake Shore Gold | |

| AR | Argonaut Gold | LYD | Lydian International Limited | |

| ASM | Avino Silver & Gold Mines Ltd. | MAG | MAG Silver Corp. | |

| AST | Astur Gold Corp. | MGT | Mines Management Inc. | |

| ATG | Atlanta Gold Inc. | MQR | Monarques Resources | |

| AUM | Golden Minerals Company | MSV | Minco Silver Corporation | |

| AXR | Alexco Resource Corp. | MTB | Mountain Boy Minerals Ltd. | |

| AZ | AZ Mining Inc (Wildcat Silver) | MUX | McEwen Mining Inc. | |

| AZX | Alexandria Minerals Corporation | NCQ | Novacopper | |

| BCM | Bear Creek Mining Corporation | NDM | Northern Dynasty Minerals Ltd. | |

| BTG | B2 Gold Corporation | NG | NovaGold Resources Inc. | |

| CDE | Coeur d'Alene Mines Corporation | NGD | New Gold Inc. | |

| CKG | Chesapeake Gold Corp. | NGQ | NGEx Resources Inc. | |

| CMB | CMC Metals Ltd | NOX | Niogold Mining Corp. | |

| CRJ | Claude Resources Inc. | OGC | Oceana Gold | |

| CUU | Copper Fox Metals Inc | ORA | Aura Minerals Inc. | |

| CZH | Crazy Horse Resources Inc. | P | Primero Mining Corp. | |

| DGC | Detour Gold Corporation | PAA | Pan American Silver Corp. | |

| DPM | Dundee Precious Metals Inc. | PG | Premier Gold Mines Ltd. | |

| EDR | Endeavour Silver Corp. | PVG | Pretium Resources Inc. | |

| EDW | Edgewater Exploration Ltd. | RMX | Rubicon Minerals Corporation | |

| ELD | Eldorado Gold Corporation | RPM | Rye Patch Gold Corp. | |

| EMX | Eurasian Minerals Inc. | SBB | Sabina Gold & Silver Corporation | |

| EOM | Eco Oro Minerals Ltd. | SEA | Seabridge Gold Inc. | |

| ER | Eastmain Resources Inc. | SGN | Scorpio Gold Corporation | |

| EXN | Excellon Resources | SMF | Semafo Inc. | |

| FR | First Majestic Silver Corp. | SPA | Spanish Mountain Gold Ltd. | |

| FVI | Fortuna Silver Mines Inc. | SPM | Scorpio Mining Corporation | |

| G | Goldcorp Inc. | SSO | Silver Standard Resources Inc. | |

| GAL | Galantas Gold Corporation | SVL | SilverCrest Mines Inc. (acq. by FR) | |

| GBU | Gabriel Resources Ltd. | SVM | Silvercorp Metals Inc. | |

| GCM | Gran Colombia Gold Corp | THO | Tahoe Resources Inc. | |

| GPG | Grande Portage Res. | TME | Temex Resources Corp (acq by LSG) | |

| GPR | Great Panther Res. | TMI | Tri Metals Mining Corp | |

| GQM | Golden Queen Mining Co. | TML | Treasury Metals Inc. | |

| GUY | Guyana Goldfields Inc. | TSN | Telson Resources (Soho) | |

| GWA | Gowest Amalgamated Res. | TXG | Torex Gold Resources Inc. | |

| HL | Hecla Silver | TVI | TVI Pacific Inc. | |

| HRT | Harte Gold Corp. | TYP | Typhoon Exploration Inc. | |

| IMG | Iamgold | XRC | Exeter Resource Corp. | |

| IPT | Impact Silver Corp. | YRI | Yamana Gold Inc. | |

| ITH | International Tower Hill Mines Ltd. |

Epilog (added June 08)

The miner bear market was long in the tooth as this article was drafted. Yet it has the merit that the very capitulation for gold and silver miners still was to follow 16 days later. After miners had been strengthening during the first few trading sessions of 2016 (when I have drafted this article), the final plunge to the bottom indeed materialized.

If the ongoing miner recovery indeed proves sustainable, the present article will continue to be a reference for comparing the present situation to that of end December 2015.

Graphs used in the latter part of this article can be compared to the present ones on the Gold Miner Pulse page or the Miner's Performance Page (Tabs below the blog title).

Gold Miner Pulse

HUI/Gold as a measure for miner strength has turned a corner with its 200 dma now in an uptrend for the first time since 2013. Nevertheless the current level (0.182) only is in line with that attained during the 2013-2014 failed recoveries (well after the April 2013 gold plunge). More than a doubling up is needed to bring HUI/Gold back in line with where it was by end 2010. Precious metals prices need to maintain their uptrend in order for this to possibly materialize.

Miner performance

Especially for the top quintile the individual miner performance indeed has improved in a spectacular way. Yet also for most miners in the lower quintiles, advances have been comparable. Just noticing the scale shift for the different graphs tells a lot.

No comments:

Post a Comment